You must log in or register to comment.

Buddy, bro, my pal, finance friend.

Nvidia went up 350% over the past year. You should have written a fake story about videogames.

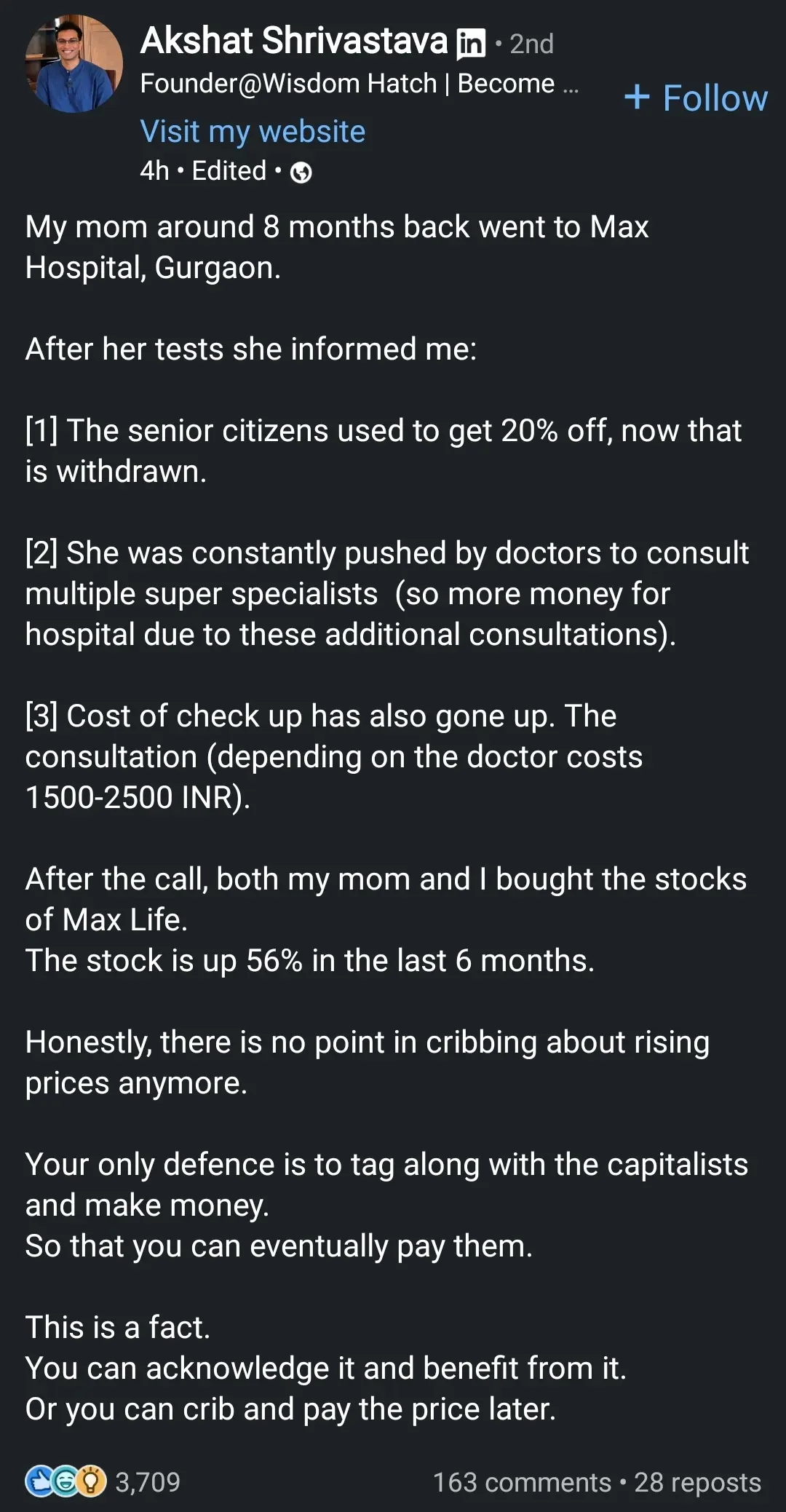

My mom around 8 months back went to Micro Center, Denver.

She needed a new graphics card. The salespeople there urged her to buy the brand new Nvidia 4090 for $1500.

She used to get free AAA games with purchase, now that was withdrawn

Damn, $1500 is actually a great price for a 4090. If only…

Edit: I don’t know how I got here. I just realized this post is 4 months old.

"capitalism is a horrible system that tried to bankrupt my family though medical expenses.

But don’t fight it, support it by giving them your money anyway, and then any that you earn after that.

You are a fool of you don’t buckle to the whims of big business"

“support it via ✨️ g a m b l i n g ✨️”

Bruh, it’s not gambling if you know you’re gonna win *taps forehead meme*

deleted by creator

Be on the forefront of the revolution!

Which means posting snarky memes

What’s extra annoying about this is that in his story, his mom gets screwed over by the hospital so rather than thinking to complain or go elsewhere he thinks ‘yah im gonna invest in that’. Investing in bad actors like that just reinforces their shitty behavior.

Are you fucking joking that a hospital is on the stock market? I know, its the company that owns the hospital, but its still fucked up. Should not be allowed.

Why not? Companies that make pharmaceuticals, prosthetics, imaging devices, etc are all on the stock market too, so if hospitals weren’t on there, you could build a portfolio to approximate it by buying producers of medical equipment.

The real issue isn’t whether something is publicly traded, but collusion between groups to keep prices high. For example, it’s mutually beneficial for insurance, hospitals, and medical equipment providers to increase costs. Higher equipment costs means care providers can charge more (what’s another few hundred when the bill is in the thousands?), and higher total bills means insurance companies can charge higher premiums (they’re usually limited to a certain percent of cost as profit). Hospitals generally don’t have direct competitors since it’s prohibitively expensive to build one and there’s lots of bureaucracy based on “need,” so you can’t just go next door to an org that’s not involved in the collusion.

Here’s some YouTube videos about it:

There are lots of viable solutions here, but banning them from the stock market isn’t going to solve anything. The first order of business imo is making everything more transparent.

The real issue is the belief that essential services should make profit. Socialized, regulated Healthcare FTW.

I disagree.

I know it’s an anecdote, but I have a coworker that shared an experience moving from Canada to the US, and they said they much prefer the American healthcare system to the Canadian system. This is from the perspective of a relatively well off individual (not rich, just middle to upper middle class), so obviously someone at the bottom end of the income spectrum would have a different opinion.

So my question for people who promote socialized medicine is this: if you could easily afford both, would you prefer socialized or privatized medicine? And why?

I think we have a cost problem, not a structural problem, so we should look at ways of reducing cost before completely changing the structure of our healthcare system. My primary concern is getting insurance away from employers, publicly funding emergency services, and making hospital costs more transparent (e.g. publicly posted price ranges for common procedures). As in, reform the current system, not replace it.

know it’s an anecdote, but I have a coworker that shared an experience moving from Canada to the US, and they said they much prefer the American healthcare system to the Canadian system. This is from the perspective of a relatively well off individual (not rich, just middle to upper middle class), so obviously someone at the bottom end of the income spectrum would have a different opinion.

The problem is that healthcare systems are meant to take care of the entire population, not just the middle class or higher. If you are a moderately healthy and wealthy person, yes the American healthcare system is fine, but that’s not exactly the what your entire system should be geared for.

The only reason they like the system is because they are the bread and butter of private insurance. Healthy working adults whom don’t require lots of expensive care. However, if they were to developed a chronic illness, or get injured or I’ll to the point where they can’t maintain their employment… That’s when you get to experience the worst healthcare experience America has to offer.

if you could easily afford both, would you prefer socialized or privatized medicine? And why?

As someone who’s had socialized medicine (Tricare) and now currently has “good” private insurance (BCBS ppo), I definitely prefer socialized.

There’s no worry that your going to catch an unexpected co-pays, you aren’t nickle and dimed for every script or visit. No worrying about out of pocket maximums, yearly deductibles, or lack of specific coverage. You don’t have to get specialized insurance for just your eyes and teeth, the benefits go on and on.

I think we have a cost problem, not a structural problem, so we should look at ways of reducing cost before completely changing the structure of our healthcare system.

The cost problem stems from the structural problem. Private insurance steals the ability to effectively collectively bargain for lower prices. It also diverts funding away from the socialized insurance pool of Medicare, which lacks the young healthy subscribers that help stabilize and fund the care for elderly and sick.

Imagine if all the money that private insurance pockets went towards actually caring for people. Imagine if hospitals didn’t have to employ a small army of managers and billing agents, just to get paid for services already rendered. Imagine the collective bargaining power that we’d all have if pharmaceutical companies knew there was only one customer in the entire nation.

You give that all away for what? A policy that goes away the moment your employer decides they don’t want to pay that much this year? A policy that ties your physical well being to your employment? A policy that terminates your coverage the very moment you need it the most?

unexpected co-pays, you aren’t nickle and dimed for every script or visit

Again, you’re talking about cost, not which you’d prefer from a service perspective.

I think there are lots of opportunities to make costs lower, such as reducing patent lengths (reduces medication costs) and simplify insurance (reduces admin costs). We should also make changes to liability law so doctors can focus on providing care. Some specific proposals:

- patents - reduce to 5-7 years; should cut costs of pharmaceuticals

- insurance - simplify and standardize coverage; coverage details and bill processing should be automated

- publicly post costs of common procedures, and give expected, average, and maximum costs before any procedure

And so on. And on top of that, expand Medicare/Medicaid a bit with costs phasing in the higher your income goes. I think we should also cap access to Medicare for retirees at a certain income level as well, and remove FICA tax caps.

We should absolutely be discouraging employer sponsored insurance and encouraging longer term insurance plans (e.g. like life insurance, you lock in at a lower rate if you sign up while healthy). Dropping someone from insurance shouldn’t be a thing at all, and the payout for doing so should be much higher than any costs the insurance company would incur by keeping them.

Again, you’re talking about cost, not which you’d prefer from a service perspective.

If you went to a restaurant and they ran separate charges every time you ordered something… You wouldn’t consider that bad service?

Also, I went to the same physician when on Tricare, so it’s the same exact service, minus all the billing hassle.

I think there are lots of opportunities to make costs lower, such as reducing patent lengths (reduces medication costs) and simplify insurance (reduces admin costs).

And I think you could do the same things and still lower the cost even more by banning privatized insurance?

Also, what is the profit motive for insurance companies to simplify their process? Their systems were purpose built to be as complicated and time consuming as possible, if they make the process easier, their subscribers would utilize it more, making insurance pay more often.

patents - reduce to 5-7 years; should cut costs of pharmaceuticals

- insurance - simplify and standardize coverage; coverage details and bill processing should be automated

And again, why would corporations do this? And how would we enforce this?

The Medicare billing is automated, and pretty simple. It’s what every insurance company has the option of doing, but only Medicare and Medicaid have automated the process. This is because private insurance companies have no profit motive to pay for their prescribers healthcare.

publicly post costs of common procedures, and give expected, average, and maximum costs before any procedure

Most hospitals have this information available, especially if you call their financial services office. In fact if you are a Medicare patient this information is publicly available on the CMS website, and they list exactly how they came to that figure.

The whole hidden ledger thing is primarily only a problem at privatized hospitals that were bought or built by private hospital networks operating for profit.

I think we should also cap access to Medicare for retirees at a certain income level as well, and remove FICA tax caps.

The inherent problem with this is that the elderly are fundamentally uninsurable. You can’t make a profit from an elderly subscriber, the cost of their end of life care will always cost more than any subscription fee they may pay in.

This is why the vast majority of private insurance do not offer primary insurance to people older than 65. The whole point of private insurance is to extract money from healthy patients and then dump them onto Medicaid if they become disabled, or onto Medicare when they begin to age and decline in health.

We should absolutely be discouraging employer sponsored insurance and encouraging longer term insurance plans (e.g. like life insurance, you lock in at a lower rate if you sign up while healthy).

Who would offer those plans, and why? The only reason most people can afford private insurance is because their employer collectively bartered for the price. A lot of people have no idea how much of their employee compensation package is taken up by their insurance, but the burden of cost is redistributed by the entire employer pool.

Dropping someone from insurance shouldn’t be a thing at all, and the payout for doing so should be much higher than any costs the insurance company would incur by keeping them.

This would bankrupt private insurance companies… I don’t think you fully understand how hard it is to make money on health insurance. The only way to do so is by withholding healthcare to your subscribers, or to offer plans with obscene co-pays or deductible.

The cost on average for full coverage is around 8.5k dollars a year for an individual, or 24k for a family. Meaning that the cost of a single operation, illness, or inpatient procedure will wipe away the potential profits from an individual subscriber for years. The only way to recover from having one I’ll subscriber is to balance them with a dozen healthy subscribers.

Without managing this equation of large healthy profitable pool vs small costly pool, the entire charade of private insurance would collapse upon itself.

One of the largest drivers in the increase in healthcare cost is these types of people. People whom don’t have any insurance, but still have healthcare needs. For these people the emergency room is typically their only option. This is one of the reasons emergency medicine is such a drain on hospital resources. For every person they treat without insurance, they have to raise the cost on people with insurance, simply so they don’t go out of business.

restaurant and they ran separate charges

It’s funny you mention restaurants, in that case I don’t particularly care when they bill me because the menu says precisely what I’ll pay (counter order vs table service doesn’t matter as much as cost and quality). If it’s market rate (steak or seafood), they’ll tell me what the day’s rate is and what cuts they have.

I don’t get that with health care, even getting a range in a quote is like pulling teeth. I pushed back a ton when my daughter needed a surgery, and after several calls I still didn’t get a clear answer, and this was for a routine surgery. The quality and speed of service was great, billing was not.

One of the benefits of socialized medicine is not having to worry about billing, but you also often get delays in care. I don’t think we need to go to socialized medicine to solve the unexpected costs issue, we can expect care providers to absorb some of the variability.

what is the profit motive for insurance companies to simplify their process?

I agree, the current profit motives are misaligned, and pushes like the ACA to further expand the number of people with insurance further entrench these practices.

The profit motive should be attracting customers who otherwise would go without. But since pricing isn’t transparent, cash payers don’t have the same leverage to get a fair price. Many care providers have an informal “cash discount,” but that’s just not the same.

If the system works well for cash customers, insurance would need to earn customers’ business, but when most people have insurance, the patient is no longer the customer, the employer is, so they’ll charge individual customers more than employers with group plans. If we separate the insurance from the employer, they would need to cater to patients.

Removing private insurance is one option, but that’s also quite disruptive and has potential for other issues (e.g. why would Medicare bother with good customer service if it’s the only option?).

Most hospitals have this information available

That wasn’t my experience. We had two options for a surgery with different risks and costs, and after several calls, we couldn’t get any numbers, just A costs more than B. That’s why I’m so interested and “it depends on your insurance” blah blah blah. That’s why I’m so interested in this. And this wasn’t some podunk hospital, it was the premier children’s hospital in the state, run by the premier public university in the state, and services kids outside the state.

I should be able to get quotes on a procedure from multiple care givers for a non-urgent procedure (like the one we had).

how would we enforce this?

Patients should be able to switch insurance if they don’t like the one they have. Right now, you either use the insurance you have or pay out the nose by giving up company cost share and ACA subsidies.

If my company offers a crappy plan, I should be able to take what they would’ve contributed and pick my own plan. If that was the case, insurance companies would try harder to make their service more convenient, just like auto insurance does (not a gold standard, but much better), and HR orgs would probably try harder to pick better plans.

You can’t make a profit from an elderly subscriber, the cost of their end of life care will always cost more than any subscription fee they may pay in.

If you’re wealthy, you don’t need much from your insurance. End of life care could be self funded, and insurance is there for the other surprises that could ruin your retirement. It would be totally acceptable for an insurance company to require some kind of down payment to cover EOL care, or a minimum number of years for coverage (if you die before the end of the contract, it counts as debt the estate needs to pay back).

their employer collectively bartered for the price

I’ve run the numbers and can get a similar price (within 10% or so) for similar coverage without ACA subsidies, but I need to factor in how much they’d contribute to their own plan. Add to that couples who both work, your options are: have separate plans (less efficient) or give up the employer subsidy.

This would bankrupt private insurance companies

No, they’d just adjust rates to compensate. If there’s something insurance companies are good at, it’s averaging costs and holding a surplus. So a company that’s better able to estimate this should get more customers and stay in business longer.

If they offer a 10-year or longer plan, they just need to average costs across their target demographic over those years to come up with a premium. Term life insurance companies do this, so why not health insurance?

For these people the emergency room is typically their only option.

Especially for homeless people. Which is a huge part of why I’m a fan of government funded ER. That’s a huge risk factor for insurance companies and hospitals, and it’s also a huge complexity for visitors and whatnot, so it should just be provided. If the paramedic thinks you need emergency care, it should be 100% free. However, hospitals should be empowered to deny care (and charge for wasting ER capacity) for non-emergencies.

But any extended care once you’re stabilized should be covered by insurance instead, because you have actual choices in your care (and could theoretically walk out if you choose not to accept further care).

The real issue isn’t whether something is publicly traded, but collusion between groups to keep prices high. For example, it’s mutually beneficial for insurance, hospitals, and medical equipment providers to increase costs. Higher equipment costs means care providers can charge more (what’s another few hundred when the bill is in the thousands?

This isn’t how pricing is set for medical equipment… Nor is high equipment cost the reason behind the pricing increase.

Every hospital that accepts Medicare utilizes CMS guidelines when it comes to billing. Medicare sets the general price for items, factoring in things like historic pricing, cost of purchase from vendor, and the price of labour required to fit or make the device function.

The complex and expensive aspect of hospital billing stems from the introduction of private insurance companies. The ones that require more paperwork and processing time than Medicare, and will attempt to make the process as hard as possible.

Hospitals generally don’t have direct competitors since it’s prohibitively expensive to build one and there’s lots of bureaucracy based on “need,” so you can’t just go next door to an org that’s not involved in the collusion.

Because hospitals are a natural monopoly, not only are they prohibitedly expensive, but it’s also extremely hard to profit from them in the long term. Which is why there’s a large amount of bureaucracy to get them built.

Pretty much every ER room in America is a huge money sink that the rest of the hospital has to economically support. You add too many hospitals, and the services that are profitable get too spread across the area to support their individual ER operations.

Which is why about 10-15 years ago there was a large push from venture capital to build “hospitals” without trauma rooms. These hospitals began to eat up all the funding in the area and began shutting down hospitals with trauma wards. This is when a lot of states adopted legislation that would help curb this behavior.

There are lots of viable solutions here, but banning them from the stock market isn’t going to solve anything. The first order of business imo is making everything more transparent.

Banning private insurance is the only thing that would lower prices for Americans. None of the issues you covered are even close to the reason why things are getting expensive.

hospitals are a natural monopoly

Not when there’s any kind of population density.

private insurance companies. The ones that require more paperwork and processing time

But what are those insurance companies processing? If you look at it, it’s “special deals” so the agents can get a bonus, it has nothing to do with actually saving their customers money. Hospitals inflate prices so they have room to make cuts so the insurance sales people feel like they’re winning.

The problem here isn’t with the nature of insurance, but the collusion between insurance companies and care providers. It’s a dance they play so everyone feels like they’re winning, and at the end of the day the customer is the one that loses. It’s not a competitive market, it’s a bureaucratic one where you have HR departments, insurance salespeople, and hospitals all propagating the current system because it’s lucrative for all of the middlemen.

Medical suppliers want a piece of the action too. That’s why we get things like insulin prices going up:

The high cost can be attributed in part to “evergreening,” a process in which drug companies make incremental improvements to their products that can extend the life of their patents, said Dr. Kevin Riggs, a physician at the University of Alabama at Birmingham Heersink School of Medicine. He co-wrote a study published in the New England Journal of Medicine in 2015 that described the century-long history of the drug.

They prevent competition through the patent and regulatory systems, and hospitals and insurance companies are fine with it because they just pass the costs on to the consumer. Consumers don’t really have a choice because most insurance comes from employers (who just pay employees less to compensate) or taxes (ACA subsidies). Nobody actually pays the full price, so the system continues.

The same goes on with medical devices, but volume is much lower so it’s easier to prevent real competition. Add to that the legal risk for choosing a cheaper product if anything goes wrong and you’ll find no incentive to cut costs.

Let’s assume we eliminate private insurance, you just change the private collusion to public collusion, and instead of middle managers getting paid in the public sector, you get political favors to keep prices high (e.g. campaign donations). Moving insurance from private to public just moves money from one pocket to another. The true solution here is to expose the collusion, not politicize it. If you want proof of this in action, look no further than the defense department in the US.

Pretty much every ER room in America is a huge money sink that the rest of the hospital has to economically support

Which is because of free riders. The solution to that problem is different: emergency care should be completely publicly funded. It’s so expensive because the hospital has to deal with people skipping on their bills and just move the costs to paying customers.

I think we should make ambulances and all non-elective care completely free, provided a paramedic recommends emergency care.

Not when there’s any kind of population density.

Natural monopolies aren’t intrinsically changed by demand…

But what are those insurance companies processing?

It’s not the insurance company that is doing the processing. It’s the hospitals, they have to hire more and more billing agents just to extract the money that the insurance has already agreed to pay.

special deals" so the agents can get a bonus

Lol, no. By “special deals” you mean 20% less than the Medicare allowable, and if you don’t agree then you are no longer in network.

Hospitals inflate prices so they have room to make cuts so the insurance sales people feel like they’re winning.

No, they inflate the prices so that when insurance companies ask for less money it doesn’t bankrupt the hospital.

The problem here isn’t with the nature of insurance, but the collusion between insurance companies and care providers.

You have no idea what you are talking about about… I’m a provider at a hospital, specializing in orthopedics and rehabilitation. I’ve never spoken to an insurance agent about pricing. That’s not how it works.

Medical suppliers want a piece of the action too. That’s why we get things like insulin prices going up:

Those are pharmaceutical companies, not medical suppliers, they are billed under completely different systems…

Also, the reason insulin pricing is so high is because Medicare isn’t allowed to barter for pricing, largely in part because it would be unfair to private insurance companies who have smaller subscriber groups.

we eliminate private insurance, you just change the private collusion to public collusion, and instead of middle managers getting paid in the public sector, you get political favors to keep prices high (e.g. campaign donations). Moving insurance from private to public just moves money from one pocket to another.

Oh yeah, I forgot how every medical system on the planet was completely fraudulent… Oh wait, nope, mainly just America.

The biggest way to improve pricing is by group bartering, which is how every other 1rst world nation pays less for medical equipment, treatment and prescription cost than the US.

Again, nothing you said was accurate, and anyone who takes it as so is now dumber than when they began reading. Please stop spreading misinformation about fields of study you do not specialize in.

Because demand and supply don’t self-regulate healthcare. How much do you value your health? How about your own life? Oh, you’re willing to pay ANYTHING to live? Even if it’s not life threatening as long as it leaves you crippled, unable to work, you may as well be dead.

As a customer the only way to be an informed buyer is to be a physician yourself. Even if a treatment doesn’t work you still get charged, no refunds!

For-profit healthcare is fundamentally inhumane and is incompatible with capitalism. The forces that would usually regulate the market are non-existant. Demand is infinite, undercutting is pointless, customers have no way to be informed.

There’s a huge difference between emergency, life threatening care and relatively routine care. For example, if I need to get a tooth extracted, I can certainly wait to shop around a bit, and living with some pain for a few days could be worth finding a cheaper solution. I can also choose between hospitalization and self-care in many circumstances as well (e.g. normal baby delivery can happen at home or in the hospital).

For those cases where informed decisions are possible, supply and demand can work efficiently. It doesn’t work as well when there’s a monopoly on care, like in an ER, ambulances, etc.

And no, you don’t need to be a physician to be informed, you just need to consult one. I may not know the practical difference between operations, but I do understand chances of success and costs, and I know how to get multiple opinions and decide from there. That works for any field, I can convert a problem from needing an expertise to evaluating experts. Tell me what expected outcomes, the chances of various outcomes, and the costs, and I’ll get a second or third opinion if I’m not satisfied.

This gets even better the more transparent things are, because other experts can do independent reviews. A newspaper, for example, can hire a physician to review posted prices for routine operations and give an idea of how realistic those costs are. Insurance companies so exactly that, so I don’t see why a private organization couldn’t. News organizations routinely consult experts on stories.

But there are areas where there’s a monopoly, and those mess up the market’s ability to regulate prices. That’s why I’m in favor of universal coverage for emergency care, but against universal coverage for other forms of care.

Inflation (when considering the rise of cost of living): 6%

Returns of investment funds my bank offers: 5%

Disposable income to use for investing: 0Yeah, the math works out just fine on this one.

Well obviously, you should have just picked a better stock. Crystal balls aren’t really that expensive you know!

And you should have picked a better disposable income.

Yeah, rookie mistake.

Investment returns of broad market: 10-15%. Don’t invest with your bank, invest with a brokerage.

That doesn’t exactly work if you don’t have money to begin with though…

Step 1. Have money

Well I guess we’re fucked.

The first rule of making money: Have money.

Don’t forget to short the stock prior to the malpractice lawsuit when mom dies

Let me just reach into thin air and pull out some gold bars so I can buy some of these stocks too, asshole

Better figure out how to turn lead into gold, and quickly!. Alchemy revival, so haaawt this year!

Big “let them eat cake” energy.

Yes this is a wonderful idea when you live in a magical fantasy world where the vast majority of people do not have any ability to invest in any stocks whatsoever.

These idiots truly just actually think everyone is slightly different versions of themselves.

Assuming constant moderate growth (compared to the historical world-wide average), with even as little as 20currency/month over your entire working lifetime (* 45 years = ~10k), you can expect to gain about ~30k through stocks.

How much you earn scales linearly with your savings rate (the ratio stays the same), so this can be scaled up or down.

Even if your ability to invest isn’t great, it’s still worth doing.

deleted by creator

So this is absolutely a capitalist horror story, but investing in stocks is one of the best long-term strategies to counter inflation. Just not so much in the short term like the OOP says, due to the heightened risk.

All shareholders are liable for the actions of the company they own and control. When a company commits a crime, the shareholders should be held personally accountable. No fines. Jail time.

I disagree. Shareholders don’t have a say in how the company is run, and buying shares in a company doesn’t really change anything about how the company is run.

I do think execs and board members should be jailed for committing crimes though. If you have a part in the decision making, you’re culpable.

I sort of disagree. It should be tackled from both sides. Shareholders do have some culpability for investing in unethical businessed and not doing enough due diligence. Your average person saving for retirement probably did nothing wrong, dumped the money in an ETF or IRA or 401k and the investment company handled it, but the investment company should have been looking at business practices and not solely stock performance.

Jail time for the decision makers. We already have a way to punish shareholders: Fines on the company. They should just stop being small fines and start at the very least exceeding the amount the company made through crime.

Jailing the decision makers will discourage crime to some extent. The temptation will still be there to pump numbers and make a lot of money. Hitting investors and investment firms in the wallet will encourage a culture of giving a shit about where you’re putting your money.

Buying stocks is not wrong and never will be wrong. There’s nothing wrong about buying shares in an unethical company, it doesn’t provide them any money, it just pushes the stock price up slightly.

investment company should have been looking at business practices and not solely stock performance.

Investment companies should merely look at the strategy of the fund. If the fund’s goal is to match a benchmark index (e.g. S&P 500), it should only look at market cap. In most cases, the practices of the company are irrelevant, that’s why you’re buying a fund.

If you want, you can buy an ESG fund, which buy companies with a high enough ESG score. I personally think those aren’t the way to go, I think you’ll have far more impact by investing for return and buying products from ethical companies with the proceeds, assuming that ESG funds trail the overall market.

So I reject the notion of “ethical investing” and instead promote ethical consumerism.

Investing in a company is, in a real sense, providing them money. Stocks aren’t pretend money totally separate from corporate finances, they are intended to provide capital for expanding a business. If it goes well, the company makes money, the value goes up, and you can sell at a profit. If it goes poorly, you can lose up to 100% of the money you spent to buy the stock. That’s why it’s “investing.” You make it sound like a dog track where the money you put in has no actual effect on the outcome of the race, but that’s not true.

Even if it were true, where is the line? If I come to you with my meth business, a proven track record, and a high potential rate of return and I just want money to help expand, you would consider that a good business? What if it’s assassination? Suppose it’s a totally legal banana company but also they moonlight in overthrowing democracies?

It may be that my literal dollar bill that I invest does not end up in the hands of a guerilla, but in helping dump money into the company I am helping enable the behavior. In this scenario, I think figuring out who is legally culpable and should have known is impractical and the risk is too high of innocent people ending up in jail for us to lock up shareholders, but losing the money invested is absolutely a risk you take when investing, and if people lost their money more often they’d probably pay more attention and it would be a net good.

Investing… it’s providing them money

Companies only get money from stocks when they issue new shares, other than that, you buying a stock has no impact. If you spend $1000 on shares, maybe the stock price goes up by a penny or so, but the company gets none of that $1000 because you’re buying from another investor.

So no, it’s not giving them money in pretty much any sense at all unless you’re making a deal directly with the board to issue new stock at a certain price.

If I come to you with my meth business, a proven track record, and a high potential rate of return and I just want money to help expand, you would consider that a good business?

That’s completely separate from public shares.

If I buy a public share of your meth business, that doesn’t give you any new capital at all, it only gives capital to the seller. That sale has an infinitesimally small impact on the share price, so you’d see pretty much no impact unless I’m buying a very large quantity. My share is also likely not a voting share, so I have no say in how the company is run.

It’s closer to buying second hand products. It provides no direct revenue to the original manufacturer, though it does slightly increase demand for their products, which could mean they might make a little more money in the future, though most likely it’s not going to change anything at all. The main difference is that, instead of products, it’s a small piece of the company, so the market value should reflect the value of the company, not the market value of a single product.

Let’s say your meth company doubles in value because you’re a real Walter White. I could then sell my share and use the proceeds to buy ad space to oppose meth. The purchase and sale has no impact on your business, but my ad space absolutely does.

So me buying shares of an unethical company does pretty much nothing to their bottom line. If I bought a single product from them instead, it would have a much larger impact than spending the same amount on a share of their stock. So the best thing you can do is invest wisely (i.e. chase returns) to grow your money and spend your gains on ethical products.

losing the money invested is absolutely a risk you take when investing

Absolutely! That’s why I shouldn’t buy Enron stock or whatever. Due diligence is absolutely important, but the due diligence should be on future growth potential (well, market sentiment about long term growth, actual growth is less important), not in ethics. If a company is doing illegal stuff, that’s a risk to long term growth since the government will likely step in.

Invest to grow your capital, and spend ethically. There’s something cathartic about making a bunch of money investing in oil and then buying green products with the proceeds.

Major shareholders only. People just trying to retire aren’t the problem.

So people with IRAs should be punished for using an investment vehicle that actually allows them to retire?

If you can’t beat em join em!

This is what I did with my banking fees…

I bought enough stock that the dividend covers my monthly fees. I reinvest the dividend so the yield keeps increasing. It’s a Canadian bank so it’s safe AF and not going anywhere and it’s up like 18%+ since I started the other year so I’m not going backwards there either.

Weird way to cover my fees but seems to be working.

This is a weird way to say “Things cost too much? Have you tried not being poor?”

I mean yeah. I also own a house and have set my life up in such a way that I can afford to live what most people consider a normal life.

I’ll be honest if you can’t afford ~$1,000 in savings. Which is the sum that it took to cover my bank fees in dividend returns then it’s not about being rich or poor, it’s about being poor with your financial decisions. I grew up poor. Literally bankrupt poor, moving from place to place as we ran from bills. I started paying for my own clothes at age 9 and foot the bill for my entire life since age 12. Having $1,000 in the bank is not just for rich people. I’ve had that in the bank since I was 15 years old. Sometimes it wasn’t any more than that, but even when I was living on my own with zero support and bills up to my eyeballs, there was still a chunk of money earning me money along the way.

Dad of 3 here, probably similar age to you.

I am well aware of how hard we had it growing up, and how much effort it took us to get anything put aside. I remember two hours travel for an extra hour of work at my second job, 3am finishes and 6am starts, and still work weekends, public holidays and up to 26 hours in a row.

I am also unfortunately well aware this is becoming the norm, and at least we had a few years where this got you a bit ahead. Its now not enough for many and I don’t know how then next generation will manage.

Life was never easy, I don’t know when the story it was got sold to people. At the end of the day, if you can’t scrape together $1000, then shits beyond fucked up and tough decisions need to be made. I didn’t take a vacation for like 15 years other than a long weekend so I could save up. That wasn’t even tough LoL, it was just life. That was the norm around me and I expect it to continue for many if not most.

I bought enough stock that the dividend covers my monthly fees.

That’s already a good bit of capital locked in stocks just for banking fees. Not saying that’s not worth it but not everyone has the luxury of having that capital.

it’s up like 18%+ since I started the other year so I’m not going backwards there either.

Note that this is mostly due to the current economic situation. As the world as a whole recovers from the pandemic, global indices rise.

With this sort of strategy, you must expect draw downs of just as much however; a crisis usually sends stock prices down faster and further than a recovery period like ours sends them up by. As an example: The start of the Palestine war last year sent the FTSE-All-World index down 5% in just a week or so.

Historically, the stock prices as a whole have grown around 7% p.a., so if the historical average growth continues, investing in a broad spectrum of stocks is a winning strategy.

{kind=link}