Traditionally, retiring entails leaving the workforce permanently. However, experts found that the very definition of retirement is also changing between generations.

About 41% of Gen Z and 44% of millennials — those who are currently between 27 and 42 years old — are significantly more likely to want to do some form of paid work during retirement.

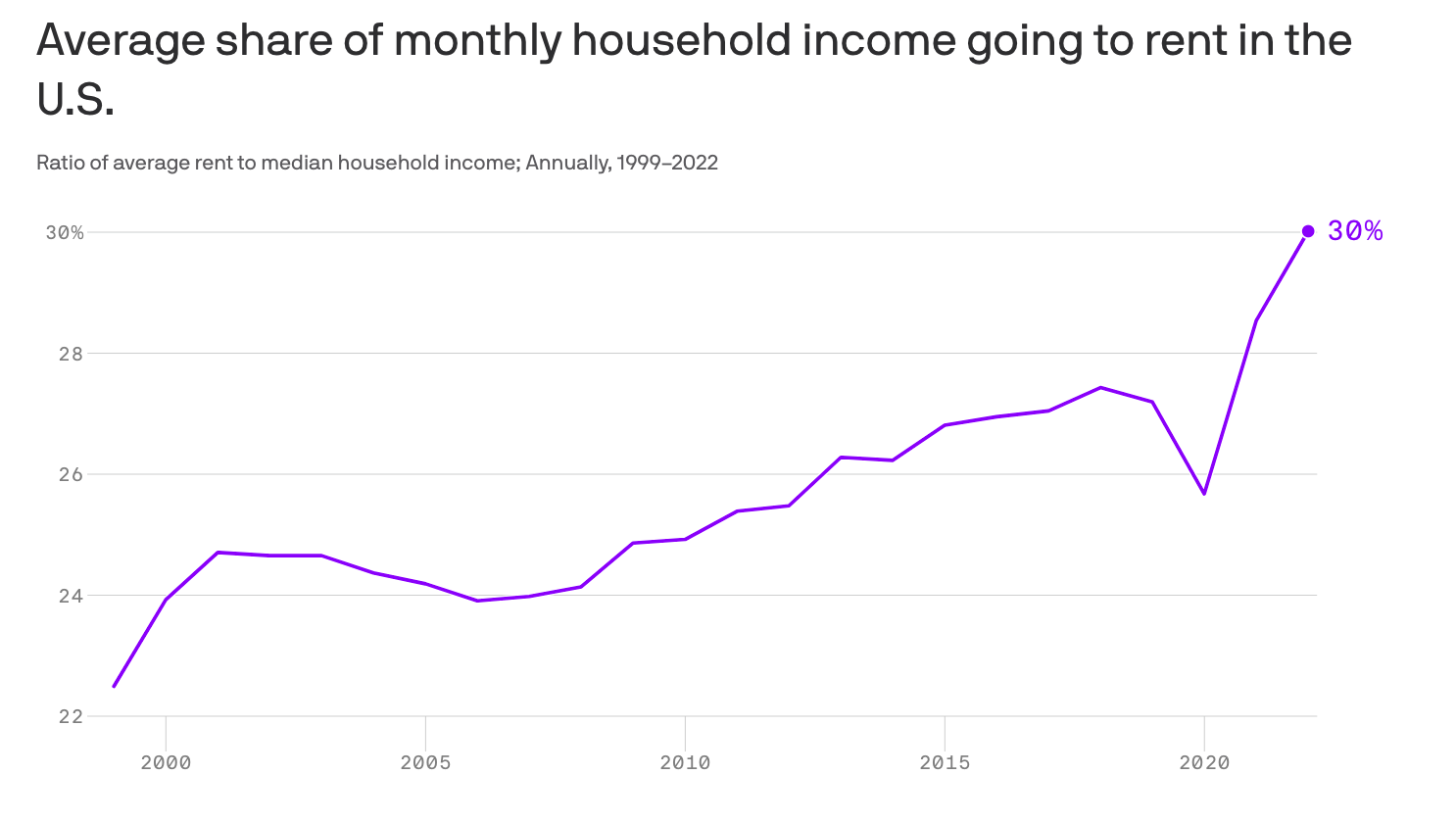

…

This increasing preference for a lifelong income, could perhaps make the act of “retiring” obsolete.

Although younger workers don’t intend to stop working, there is still an effort to beef up their retirement savings.

It’s ok! Don’t ever retire! Just work until you die, preferably not at work, where we’d have to deal with the removal of your corpse.

Maybe, just maybe, Gen-Z is not saving as much for the future because (1) they have less money to save due to inflation, and (2) they don’t foresee a viable future. These reasons can also explain the parenthood rate dropping lately.

Main reason I never had kids was I was screwed over by just about everything financially. Student loans, housing/“financial crisis”, medical system, deck stacked against self-employment, predatory credit cards. Great job, USA. Then the same cunts who did that bemoan low birth rates and cry about immigrants.

There are TOO MANY procedures/fees/tax/unsafe ways to lose everything you have or be in a position where you will never be able to live without constantly being demanded to provide more work/cash/time.

Agreed, life wasn’t this shakey in the past. Depression era: certainly, but it was caused by the same BS we are dealing with now. For example, it’s amazing that medical bills are a leading cause of bankruptcy and thus degradation of quality of life in the US, and there’s little will among politicians or citizens to do much about it. You could save up enough money to retire, even have good insurance, and then be screwed because you or any member of your family had a severe illness or accident, and lose everything.

Even if you make it to 65, Medicare Hospice at the end of your life is designed to wipe you out. So no inheritance…

Right, The hope for Gen X/Z has been “just wait until until your boomer parents die! Then you can have a normal life!” and then it’s oh, sorry, guess you have $4 million in medical bills if they don’t just die instantly.

Despite all that, things are overall better than previous generations. There is and always has been bad news. Life has always been a constant string of disasters, yet when you pause for a moment to reflect you realize that despite the bad news, overall it wasn’t that bad.

In many countries, yes. People in India and China for instance are on average more likely to not be in severe poverty and subsistence vs 40 years ago, though western-style modernization has caused it’s own problems. However most people are less well off in the US than we were in the 50s-90s. Reagan economics seems to have been ‘wait, why are we letting the middle class exist? We could just keep all their money’. Seriously though i was completely fucked over by what I mentioned and it’s only based on luck that I’m not homeless.

Most people in the Us are better off than the 50’s-90’s. They may feel worse off, but that is not an objective measure.

There are lots of objective measures. is one for you.

is one for you.

The argument of people being ‘better off’ now is that technology is better and more available. It is much cheaper to buy a big 4k flat panel tv now than a black and white tv with four channels and no remote back in the 50s. We have the Internet, smartphones, better health care, video games, music, streaming services, cheap air travel, food from all over the world, robot vacuum cleaners, air conditioning etc. etc.

What we don’t have so much of is cheap housing, good secure jobs, any reasonable degree of income equality etc.

deleted by creator

You must be cherry picking. 3rd world life expectancy is a lot worse than our, while we are very close to the best. If you cut the chart off below us we look bad.

Right, so my question is whether quality of life or satisfaction has improved. I’d say it has not.

Go find old newspapers and read letters to the editor. The exact problems were different ,but the same ideas .

Sure. That is the position I was speaking from.

Are you fucking high?

Unlikely. Getting high is more often associated with realizing that shit is fucked.

When people could afford a decent home on a single job paid minimum wage? Not so sure.

If you were white, sure. Less likely otherwise.

Okay, fair point that racial equity and access to opportunity has increased significantly in most of the country. Gender equality has come a long way as well, though it’s also a “ha ha you have to work now too and your family is still worse off than it was, good luck with paying for day care”

Which was a huge bullshit injustice which need correcting and hurt a lot of people.

But now we’re at the point where skin color doesn’t matter in this scenario. Only bank balances matter. And you probably don’t have a high enough one to afford a house no matter what color your skin is.

https://apps.urban.org/features/wealth-inequality-charts/

I saw a report that someone my age will need $3m to retire at 65. The average total income from 22-65 for people my age is around $1.4m. So I guess we never get to retire.

Compound interest might get you to that goal, maybe, if you start saving now.

The “start saving now” part is the bit that fucks most people.

If inflation is as high as it currently is compared to the collected interest it does not matter how much compounding is done, the buying power of that savings will flatline. Add to this equation the need to eat and live now, the amount most put away is minimal and when something comes up even those meager savings are wiped out.

The math in most households is not working out. Debt is becoming peoples rainy day fund, people are unable to even pay their property taxes with the now insufficient government minimum pensions (and a lot of people don’t think these pensions will even be there when they are eligible). This leaves people selling things (reverse mortgage, downsizing, moving to lower COL areas, etc) taking on debt to live now and generally giving up.

If you put away $50 a week for 10 years you end up with (based on a generous average 2% rate) $28,554.34. This seems like a good amount but keep in mind that you put $26,000 into this. That $2554.24 does not beat the loss of buying power over 10 years. You need much closer or better returns vs inflation for this to work in your favour. I was once told that you would be better off buying some raw metal like lead, or copper as the return on simple materials at least keeps up with costs.

You’re absolutely right, but I’ll just point out that superannuation (pension) funds in Australia are hitting 8 percent annual returns over a 30 year timeframe. You need a broader investment base to do that, and that’s hard for individuals to do by themselves. How do you diversify your $50 a week investment to maximise return? You can’t.

Here, superannuation funds do all the heavy lifting for you, it’s mandatory for employers to put a nominal amount of each pay into one. There are no minimum investment amounts with them and fees are waived if the balance is below a few thousand, so even if it’s $10 a week you get something back eventually.

So it’s possible to have it work if your government sets things up right.

Oh I am not saying people should be the ones wholly responsible for their retirement portfolio, and congrats for having a competent government pension option. I would love to have access to something better then the market equivalent of roulette.

Hell in Canada the pension plan (that you can not get enough to live off at the moment) got a stunning 1.3% return this year. And unlike other plans you need to pay extra for 40 years to get additional funds at the end (no one I know of even thinks of doing this). And some parts of the county want to spin off there own pension plan (Alberta) even though most expect it to perform worse (due to a smaller investment base and using a bad private firm to run it).

When over half of Americans live paycheck-to-paycheck, saving is not even a possibility.

It seems that a lot of things in the US are carefully designed to keep you in servitude to your current employer, which I find a little ironic coming from the land of the free.

Where I live, Australia, employers are required to put in approx 10 percent of an employee’s full time wages into a superannuation fund. This is linked via reportable wages to the tax office and companies will eventually find themselves under a lot of unpleasant attention from the Australian Tax Office if they don’t make regular payments for you.

This is basically “invisible” to workers, it’s essentially factored into the cost to have an employee by the business.The superannuation fund can be a “default preferred” one selected by the business, or an employee nominated one, and you can transfer/roll over your accumulated funds between any superannuation fund you like as you hop between jobs. You can draw from it in some specific dire circumstances, but usually you can only access it at retirement age.

For most Australians it ticks over in the background by itself. Most super funds easily beat inflation by a fair margin most of the time, and definitely in the long term. The tax office keeps track of balances for you and gives you an easy way to see what’s where and the option to roll any scattered amounts into your current main superannuation fund.

You can also contribute extra to your super fund and there are tax benefits if you do. The government actively encourages investment in super, because that way they don’t have to provide much in the way of old age pensions come 2050 or so when all workers will have some sort of decent retirement amount.

Is there any form of “mandatory” saving like that in the US? I know you guys have company pension plans of some sort, is there a government version?

That’s essentially what social security is (except you can’t access it until retirement), but it’s constantly being attacked with death by a thousand cuts, so most people under 50 don’t really expect to see much of a return.

It’s pretty much the opposite in Australia with our setup. Those starting work now will end up with the required 3-ish million at retirement if they work the standard average job here for most of their life.

But I think what you refer to as “social security” is the government “aged pension” here which is about $550 a week or so. That’s enough for a pensioner to live a very modest lifestyle here if their accommodation has been sorted previously.

It’s also suffering the same kind of squeeze you mention and is means-tested on a sliding scale so the more you can afford not to have it, the less you get of it.

Right now most boomers are on the aged pension to some degree because superannuation schemes here only really kicked in during the last 15-20 years of their working lives so they didn’t have much of a balance.

Probably in the next 30 years or so only the truly destitute will be able to get it and the rest of us will have to rely on what we’ve saved.

Do you get the pension if you don’t put into the system? I was self-employed for years, and didn’t pay into the social security system for those years because I really couldn’t afford to since my business was so modest and I was the only employee. So my SS payout will be minuscule, whereas my wife, who has worked for public libraries since leaving university, will get a small but useful if not survivable check every month. So basically if you don’t pay in, you don’t get to have a retirement pension from the government.

I’m lucky because I stand to inherit a sizable amount of money when my mother passes away that I can save for retirement, but most people aren’t that lucky and will have to live on scraps.

Yes it’s paid for via general income tax here in Australia, not something you pay into yourself per se. So, just like our public health system, even if you never worked you still get it.

Which is why the government set up superannuation schemes in the '90s because they realised a pinch point was coming down the line in the 2030’s or so. At that time there would have been too many people on the pension for it to be sustainable.

savings interest rate was less than 0.1% for about the last 10 years so even thats not looking too solid

There is no magic number you need. $3m will get you some lifestyle. You could retire at 40 with only $300k if you want to live the lifestyle that means (move to very low cost of living area where you walk to groceries). And there is a good chance social security will continue to provide a minimal income once you reach whatever age.

Not enough income to live indoors, but income nonetheless

I know places in the us where it is enough. Towns with populations of 500 are generally cheap. Not much to do in them.

You’re right. In a 1 bedroom in a rural city in a low cost of living state living as a freegan who never needs anything like medications you might be able to live off that.

I for one think that the situation with social security is that my parents and grandparents took one of the best things my country ever did, robbed it blind, and pissed all over it. Fuck. That. Shit.

And yeah I’m prepared to work the rest of my life until I get too old to work and then die homeless. That’s not what people should live like. We had something beautiful and let it fall into disrepair

I said you could. That you wouldn’t want to is my point.

Let’s say optimistically that you die at 70. That’s 30 years living on 300k, so 30k per year on rent, food, utilities and medical. You could live indoors for that amount in some parts of America in 2023. But what about in 2053? Inflation could have a huge impact on your cost of living and if you’re already living close to the bread line it’s hard to find savings anywhere. You could put your money in stocks but likewise you’re at the mercy of the market. It might be fine but if the market tanks when you’re 65 you could be in big trouble.

$300k ÷ 30yr = $10k/yr

To put it in perspective, working minimum wage ($7.25/hr) full time would earn around $15,000 in a year.

Historically no young generation has saved a lot. It is when you get older you realize how much it matters.

People who grew up in the Great Depression did. Silent generation remembers that…

Also Millennials are (historically) huge savers from living through multiple downturns.